September 5, 2025•3 min read

The Elder Care Reality: Why Estate Plans Must Include Lifetime Planning

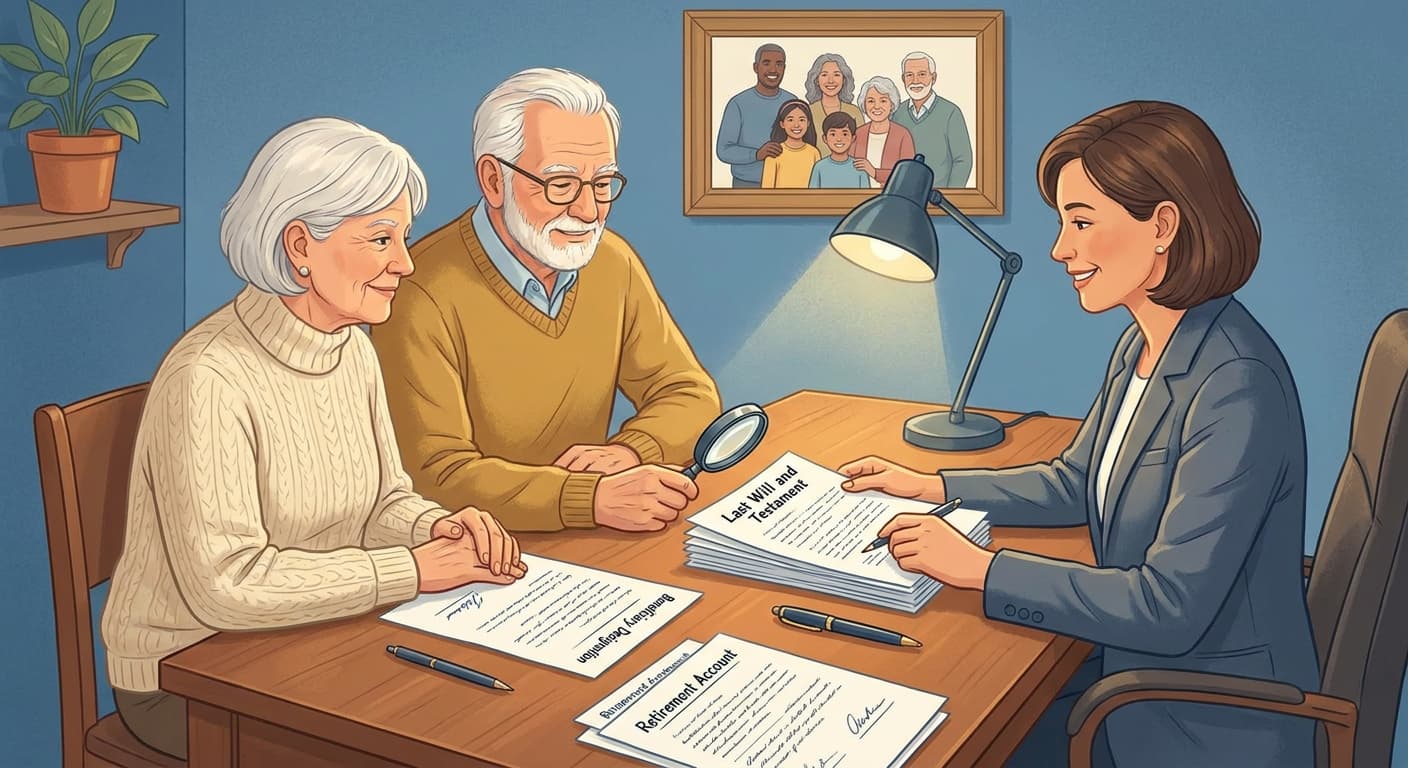

Estate planning isn't just about what happens after death. Learn why proactive lifetime planning—covering incapacity, healthcare, and long-term care costs—is essential to protect your family and assets.

Faith Otutu

Author