August 26, 2025•5 min read

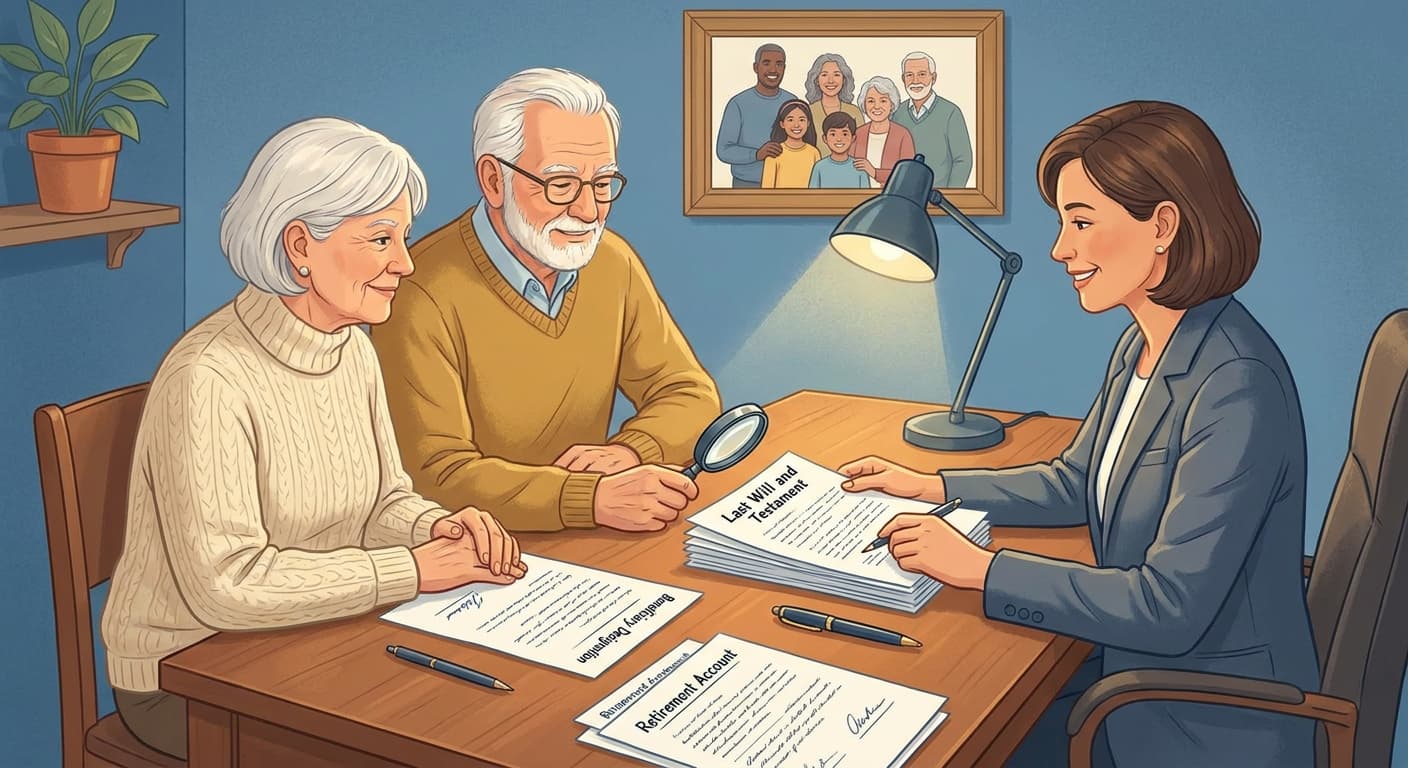

Common Estate Planning Mistakes and How to Avoid Them

Estate planning protects your family, preserves wealth, and ensures your wishes are honored. Learn the most common mistakes people make—and practical steps to avoid them.

Faith Otutu

Author